Written by Asi de Silva CFA | April 9, 2025

As I finalize this newsletter on Tuesday afternoon, markets struggled to sustain a strong start following positive momentum on tariff discussions with Japan. At its peak today, the S&P 500 was up ~4%, but closed down 1.5%.

It’s hard to pinpoint an exact piece of disappointing news today, but the escalation with China remains a concern. Both the US and China believe they have the resources to stay the course, which will make both sides worse off in a prolonged standoff.

In our view, one of the biggest differences in staying the course is the fact that China does not have elections. The President’s approval ratings are starting to flag and Republican lawmakers are making the slightest of disapproving noises. Expect this to increase if polls weaken further as consumer wallets are pinched.

Below are our brief thoughts on the markets and economic conditions since our last update on Friday.

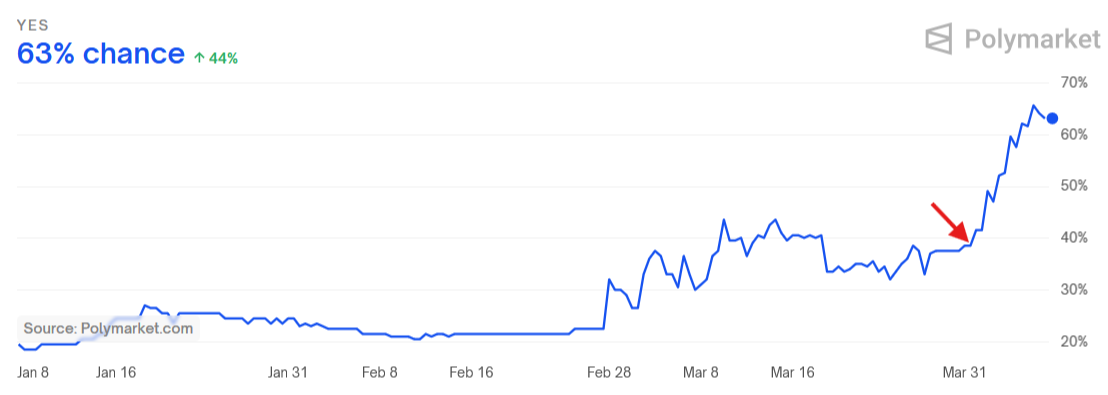

Recession Risk Has Increased

The chart below from Polymarket shows the jump in recession risk since the April 2nd (red arrow) tariff announcement. Just like expectations of Fed rate cuts, this measure partially responds to stock prices and can be adjusted if stocks continue to recover.

The Fear Index (VIX)

For those of you who follow the markets closely, you would notice the VIX, or the fear index, has increased to over 58 over the past few trading sessions. Under normal circumstances, the VIX is usually around 20.

Why is this important? It indicates the markets were in clear panic mode.

At the very least, this also tells us it wouldn’t be a good time to sell, as we would essentially be succumbing to the panic.

What’s even more curious is the performance of different market sectors over the next 500 trading sessions. See the chart below for details. As an example, when the VIX is over 50, Consumer Discretionary and Technology stocks returned 108.90% and 80.29%, respectively, over the next few years.

Source: thestreet.com

Source: thestreet.com

The Bullish Argument

Imports to the US account for 14% of Gross Domestic Product (GDP). A 10% tariff (assuming lower negotiated rates) would have a minimal negative impact on the economy. This has been the talking point for the new administration's economic policy team from day one. They also assert that deregulation will improve the 86% of the economy that is domestic activity, which will lead to stronger growth.

This assumes that other nations will play along with the US and accede to Washington's demands. China has already shown us that it will not and the President looks ready to escalate further.

Taking all of this into consideration, it’s hard to see how the market volatility will subside over the next few or even several trading sessions.

What’s next for us?

We have many other thoughts on the markets that can benefit you in both the short and long term.