Written by Asi de Silva CFA | May 1, 2025

This week we are highlighting some of the recent economic data, and unfortunately, it is worsening.

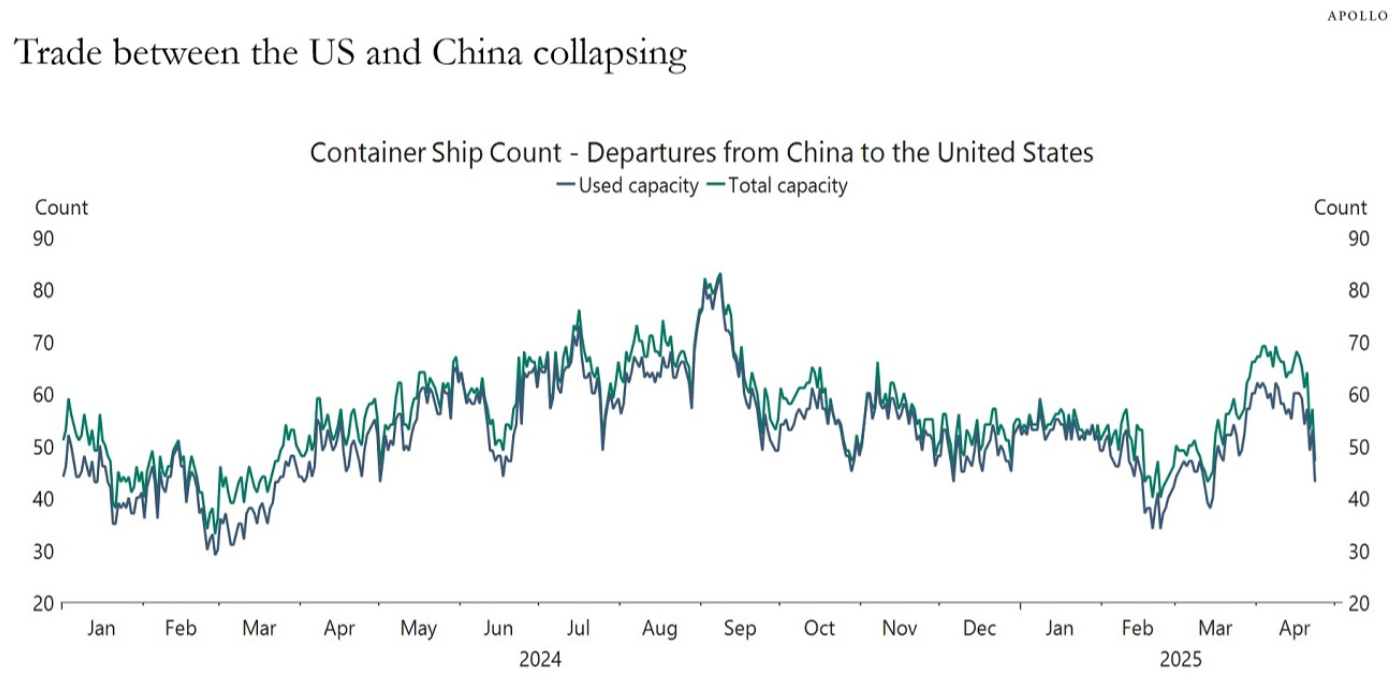

We aren’t particularly worried about the weak 1Q GDP because that was anticipated due to imports surging ahead of tariffs. We should expect stronger 2Q GDP as imports stall (see shipping chart below) and consumption spikes as consumers bring forward purchases ahead of higher prices.

We end with implications for retirement portfolios as economic uncertainty stays elevated.

Please note that nothing in this newsletter should be considered investment advice. Always conduct your own due diligence or consult with a financial advisor before implementing any strategies discussed here.

What’s the latest data?

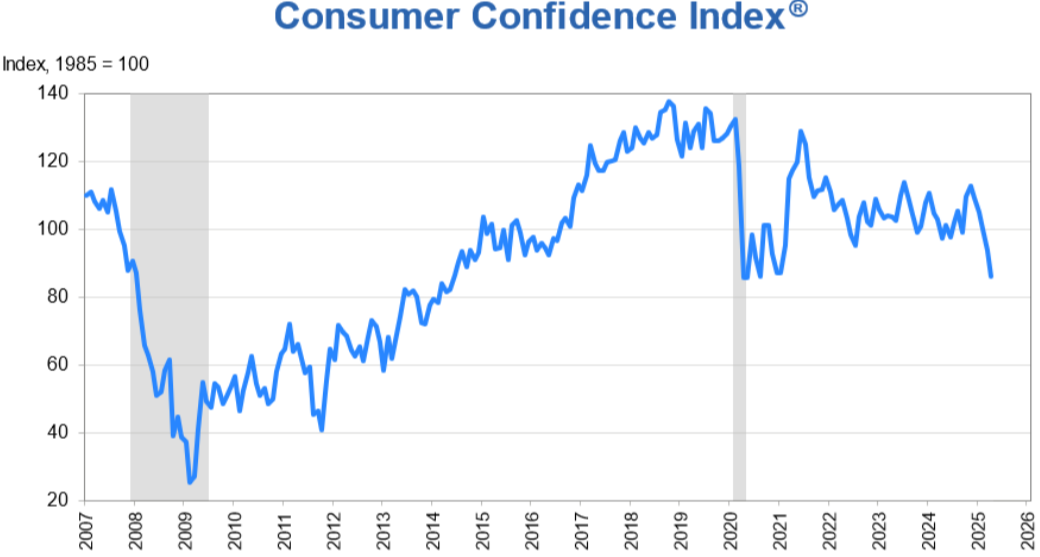

The Conference Board’s April Consumer Confidence Index dropped sharply to levels not seen since the Covid pandemic lows. You can access the chart and more details about the survey here.

Is the weakness a new development?

This adds further evidence of the consumer angst that was already visible in the March University of Michigan consumer sentiment survey. US consumers are worried even before we have seen a meaningful price impact from tariffs.

Price hikes are coming; retailers have cancelled orders,which is reflected in the sudden drop in container ships sailing from China to the US. Supply chains work with a lag and I expect both higher prices and empty store & Amazon shelves. The chart below is from Apollo Global.

Are companies feeling any better?

A majority of companies are also reacting to the uncertainty by withdrawing 2025 financial guidance, as highlighted by this Wall Street Journal headline. Many of these companies are announcing lower capacity/output and cost cuts.

Any bright spots?

I look for bullish stories daily to ensure my views aren’t myopic.This week, I was surprised by the upbeat headline below from cruise company Royal Caribbean.

Royal Caribbean is an outlier because airlines – also exposed to highly discretionary vacation spending – have either lowered or withdrawn 2025 guidance. So, there are occasional bullish stories, but they are vastly outweighed by a more worrisome lack of clarity for the corporate sector.

The administration is clearly hedging a weaker economic outcome by blaming Jay Powell at the Fed for not cutting interest rates and former President Biden for the ailments in 2025. We expect more policy volatility ahead, which will make corporate investment decisions difficult.

How does this impact your retirement portfolio?

We started 2025 with the view that US stock returns are unlikely to repeat their performance of the past decade. This meant starting the year underweight US tech, which we have further moved towards US large-cap value during the past few months.

We have modestly increased our allocation to international stocks due to low starting valuations, fiscal stimulus in Europe, and investor positioning. This is an area we could increase allocations in the coming months.

In fixed income, we are diversified between short-term Treasuries (for yield), TIPS (for inflation protection), and intermediate-term Treasuries (as a recession buffer). The risk-reward for high-yield bonds is unappealing given the economic uncertainty and low credit spreads.

We started the year with significant commodity, which included precious metals like gold. That has cushioned portfolios and we continue see value as a portfolio diversifier and safe haven asset. Bitcoin offers similar characteristics, in our view.

In general, illiquid alt funds are also unappealing as most hold economically sensitive assets, even if the private fund wrapper provides an illusion of low volatility.

Again, these broad general views are not intended as financial advice. For that, you need to speak with YOUR advisor about your specific circumstance, goals and risk tolerances.