Written by Asi de Silva CFA | April 15, 2026

I have stayed relatively quiet on markets these past few weeks, not because there was nothing to say, but because there was too much noise and too little signal.

When you combine a highly financialized world with policy made via social media and a shooting war in the Middle East, weekly market commentary risks adding to the fog rather than clearing it.

This letter is my attempt to cut through.

The short version: markets have moved from panic deleveraging to buying the dip once again. The S&P 500 is above where it was when the shooting started even as energy prices remain elevated.

Continued high energy prices are a key swing factor between US and international allocations. Gold and Bitcoin remain strategic holds despite the volatility.

Crude futures are signaling that the market believes this conflict will be short-lived, even as physical markets indicate much higher prices.

While Iran and oil dominate short-term prospects, we remain constructive on the long-term view as technology innovation diffuses.

What surprised us and why

The most telling market signal in the early weeks of the Iran conflict was not what sold off. It was what sold off together.

Defensive sectors like consumer staples and healthcare fell alongside risk assets.

Gold dropped more than 15% from its highs even as uncertainty spiked. This is not how those assets are supposed to behave.

Deleveraging is one reason. In a highly financialized world, leverage is everywhere. When volatility spikes suddenly, sophisticated funds are forced to reduce borrowed positions quickly, and they sell everything, especially what has worked.

The best performers of the year become the source of funds.

Today, the S&P 500 is signaling that the coast is clear. We think that's premature, even as we agree the ceasefire was a clear marginal positive.

We continue to believe US election polling will drive de-escalation, and markets have priced that rapidly.

The Treasury Market Has Sent a Tentative Signal

Short-term yields have risen as rate cut expectations have been taken off the table, while long-term yields have moved less.

This flattening of the yield curve could suggest the market is beginning to price in higher inflation without a corresponding rise in the growth outlook, a stagflationary read.

We hold that interpretation loosely, however. Several weeks of trading is not enough to draw firm conclusions.

The macro theme for Treasuries, in our view, is that US debt-to-GDP is near an all-time high, with little political appetite for addressing rising deficits.

President Trump’s request to increase defense spending by `50% in the next budget reinforces the issue.

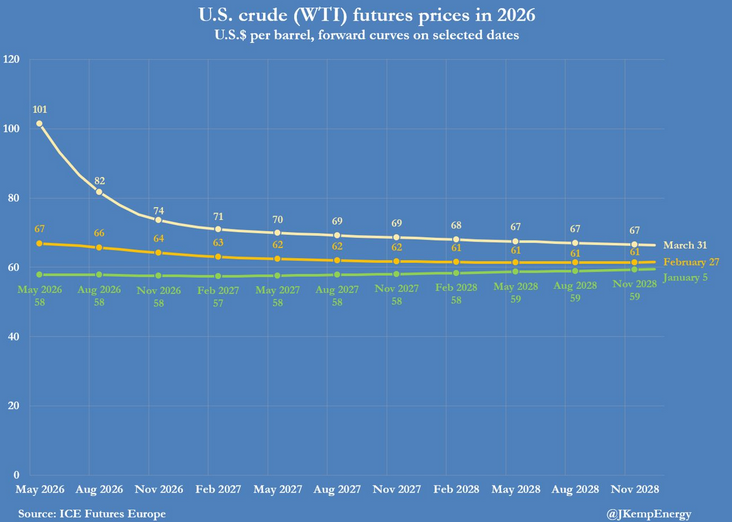

Crude Futures Are Not Buying the Fear

Spot oil prices spiked hard after the attacks, as expected. What is more interesting is what longer-dated futures are saying. December 2028 WTI crude has risen only about $6 per barrel.

Traders pricing contracts years out are not positioned for a prolonged conflict.

Source: JKempEnergy.com April 2nd

Maybe they are right.

But we hold two observations in tension: producers need higher long-term prices to greenlight new field investment, and sustained prices above $100 per barrel historically destroy demand over time.

This is part of why our energy exposure is intentionally broad, including lithium and nuclear/uranium alongside traditional sources.

Natural Gas Is a Bigger Problem for the Rest of the World Than for the US

European LNG prices have nearly doubled since before the conflict, moving from roughly $30 to ~$50 per MMBtu. In contrast, US prices have remained under $3 except for a brief spike to ~$7.

American consumers are largely insulated from the direct impact of these higher prices. European and Asian consumers are not.

This is one fundamental reason to possibly reassess the international broadening trade, even as we recognize that non-US equities still look attractive on positioning and valuation.

The Incongruous Moves

Two observations that do not fit the usual narrative:

Uranium spot prices have declined since the war started. This makes little fundamental sense. Nuclear is a primary beneficiary of an energy security environment, and long-term demand is clearly growing.

Bitcoin was the other surprise, in the opposite direction. It had already sold off sharply before the conflict began, washing out speculative positioning. As a result, it has been stable to modestly higher since the attacks.

This is a clean example of how prior positioning shapes short-term price behavior more than typical correlations.

Where We Stand

On gold: after a 65% rise in 2025 and another 20% gain into early 2026, crowded positioning amplified the selloff. We see this as noise within a structural story.

Gold and Bitcoin both serve as insurance in a world of excess sovereign debt and increasing geopolitical fragmentation. That thesis has not changed.

On international vs. US: we entered the year constructive on international markets, and the fundamental case on valuations and positioning still holds. These stocks fall the most from the 2026 peak and entered bear-market territory briefly.

That said, elevated energy prices are a real headwind to that trade. We are watching closely and will adjust as the energy picture evolves.

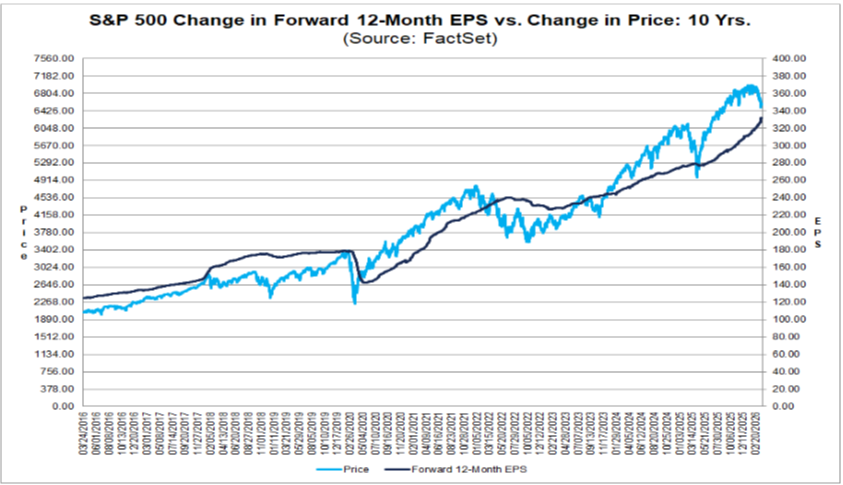

On S&P 500 earnings: estimates continue to rise (dark blue line in the chart below), which is the bull case. But we are cautious about extrapolating the post-COVID margin expansion.

With job growth modest, real incomes under pressure, and input costs rising, the ability to pass through price increases without volume loss will be a challenge.

Source: Factset

We expect the bond market to read the tea leaves first, and better than stocks. The deleveraging phase, when all bonds sold off, is over, and we expect a cleaner signal from Treasuries going forward.

Peering further into the future, President Trump's 2027 budget request includes a greater than 50% bump in defense spending.

That may test the Treasury market's desire to provide low-cost funding as the US deficit continues to increase.

What Does This Mean for You?

The Iran conflict is not just a geopolitical event. It is a macro stress test, particularly for the coming year.

A prolonged war and high energy prices will have economic consequences. US consumers have been spending beyond what income alone supports, drawing down savings.

This K-shaped economy is a fragile foundation for growth.

We are, however, constructive on the longer-term (2-5 year) outlook, as technology diffusion and productivity growth have the potential to accelerate growth.

To be clear, this is a broad macroeconomic viewpoint and not an endorsement of individual companies or sector investments, which are more nuanced.

Your financial plan includes appropriate buffers, and we are actively working through portfolio implications rather than reacting to headlines.